Wire Discount vs Financing Cost

By Josh Allen, Co-Founder — YourDiamondGuys.com Josh has over 25 years of experience in the global diamond trade, sourcing from Mumbai, Tel Aviv, and Antwerp, and has supplied diamonds to Tiffany, Cartier, Harry Winston, and more.

Most people look at the monthly payment and miss the part that matters.

That is how bad diamond pricing decisions happen.

A wire discount lowers the sticker.

Financing lowers the pain today.

Those are not the same thing.

Your job is simple.

Compare the real total. Then compare the risk.

Wire discount vs 0% financing: which is cheaper?

A wire discount is cheaper when the savings beat the wire fee and you were going to pay in full anyway.

0% financing can be the better move when keeping cash on hand matters more than a small upfront discount.

Do not compare the headline.

Compare the all-in number.

The 60-second comparison

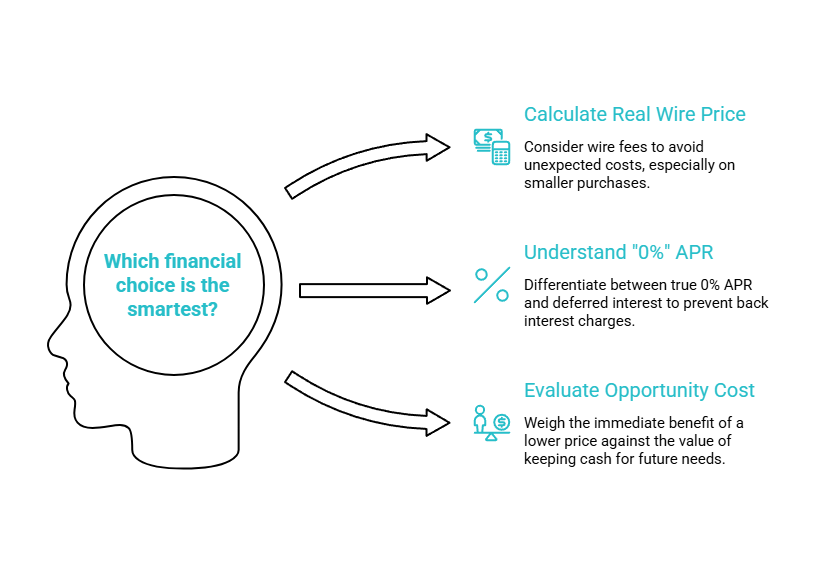

1) Calculate the real wire price

Real wire price = (Listed price × (1 − discount %)) + wire fee

Wire fees are not a rounding error.

On domestic outgoing wires, big U.S. banks often land around $25 to $30, according to Bankrate.

That matters more on a $5,000 purchase than on a $30,000 one.

2) Check what "0%" actually means

This is where people get trapped.

A true 0% intro APR offer is one thing.

A deferred-interest offer is another.

They are not interchangeable.

The CFPB explains that "no interest if paid in full" can trigger interest back to the purchase date if you miss the payoff deadline or break the payment rules.

Same "0%" vibe.

Very different risk.

3) Decide what your cash is worth

A lower price today is not automatically the smarter move.

You are giving something up when you send the cash now.

The St. Louis Fed defines opportunity cost as the value of the next-best alternative you give up when you make a choice.

That could be your emergency cushion.

That could be breathing room.

That could be the ability to say yes to something else next month.

When the wire discount is actually worth it

Wire is clean.

Lower price. One payment. Done.

Use this quick test.

| Diamond price | Wire discount | Discount dollars | Example net savings after a $30 wire fee |

|---|---|---|---|

| $5,000 | 1% | $50 | $20 |

| $10,000 | 2% | $200 | $170 |

| $30,000 | 2% | $600 | $570 |

That table is not there to impress you.

It is there to calm you down.

Small discount. Small purchase. Small win.

Larger budget. Same fee. Bigger payoff.

Same 0% claim ≠ same financing deal

If financing is truly free and you finish on time, it can be useful.

But sellers do not absorb payment-plan costs for fun.

The U.S. Chamber notes that buy now, pay later transactions can cost merchants anywhere from 1.5% to 7% of the purchase amount.

That is one reason a wire price can be sharper.

One payment method can cost the seller less.

That savings may get passed to you.

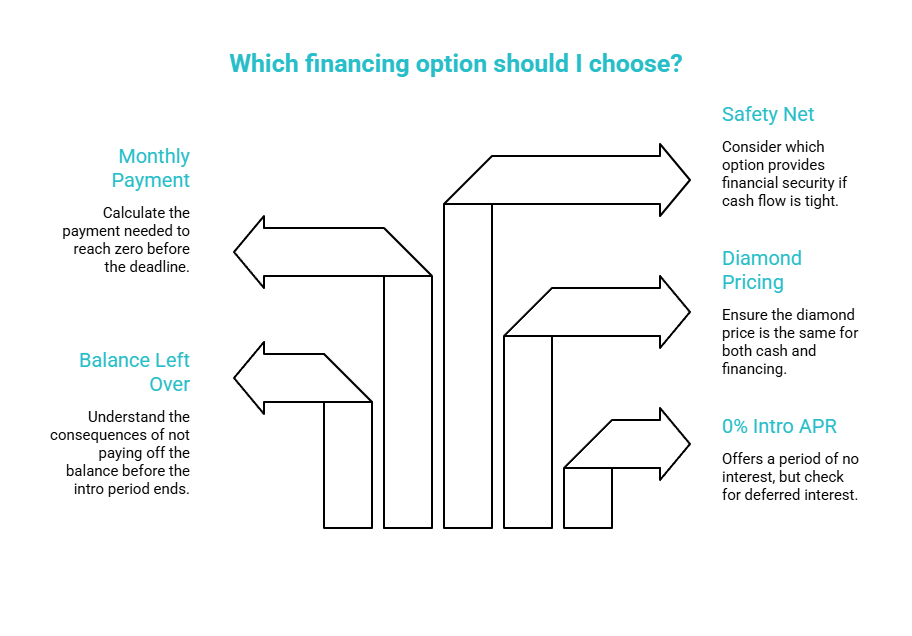

Compare the decision through three lenses

1) Total dollars paid

What is the most you could pay if life gets messy?

Not if everything goes perfectly.

If life gets messy.

That is the number that matters.

2) Cash flow

A lower total does not help you if it leaves you tight.

If paying cash drains your cushion, the "discount" can feel expensive fast.

3) Risk

Financing only stays cheap when you hit every condition.

If that feels shaky, wire may be the calmer move.

The break-even test

Turn the wire discount into an APR-like number.

Use this rough formula:

Equivalent annual rate ≈ (Wire discount % ÷ months financed) × 12

Example:

- Wire discount: 2%

- Promo term: 12 months

- Equivalent annual rate ≈ 2% per year

This is not a legal disclosure.

It is a decision tool.

It gives you a baseline.

The fine print that matters

Payment claims need clean disclosures.

That is not optional.

Under eCFR, Regulation Z says that if an ad states a finance-charge rate, it must be shown as an annual percentage rate, and required disclosures must be clear and conspicuous.

Before you choose, check these five things:

- Is it true 0% intro APR or deferred interest?

- What happens if a balance is left at the end?

- Is the diamond priced differently for wire and financing?

- What monthly payment gets you to zero before the deadline?

- If cash gets tight, which option still feels safe?

Free Diamond Consultation

Numbers on a checkout page can look clean.

They are not always honest.

If you want a second set of eyes before you commit, book a Free Diamond Consultation.

We will help you compare the wire savings, the financing cost, and the real risk.

Then you can choose the option that protects your budget.

And your peace of mind.

Questions? Reach out directly for a free consultation, or drop them in the Diamond Buyers Academy community — Rob and I answer personally.

Frequently Asked Questions

*Some links on our site may earn us a small commission at NO EXTRA cost to you, helping us keep our content free*